Understanding What is a Family Budget: A Clear Guide

A family budget sounds simple enough and millions of American households create them every year. Yet studies show that more than 60 percent of families still struggle to pay their bills on time or save for emergencies. Most people think budgeting just means cutting back, but the reality is different. A smart family budget is actually about making your money work for your goals and giving your household more freedom, not less.

Table of Contents

- Defining A Family Budget: Key Concepts

- Why Family Budgets Matter For Financial Health

- How A Family Budget Works: Basics Explained

- Components Of A Family Budget: Income And Expenses

- Real-World Examples Of Family Budgets In Action

Quick Summary

| Takeaway | Explanation |

|---|---|

| Understand your financial landscape | A family budget provides a clear overview of income and expenses, helping families make informed decisions. |

| Align spending with family goals | Creating a budget empowers families to prioritize their financial objectives and reduce unnecessary expenses. |

| Regularly review and adjust your budget | A dynamic budget should adapt to changing circumstances and financial goals to remain effective. |

| Involve family members in budgeting | Educating all family members on budgeting promotes transparency, responsibility, and long-term financial literacy. |

| Create a safety net for emergencies | Budgeting helps identify and allocate funds for savings, ensuring financial stability during unexpected challenges. |

Defining a Family Budget: Key Concepts

A family budget is more than just tracking money. It’s a powerful financial planning tool that helps households understand their financial landscape and make strategic decisions about spending and saving. Understanding household financial management requires recognizing how a budget serves as a roadmap for your financial journey.

What Exactly is a Family Budget?

At its core, a family budget is a detailed plan that outlines your household’s expected income and anticipated expenses. Think of it like a financial blueprint that shows exactly where your money comes from and where it goes. This comprehensive overview allows families to:

- Track total monthly income

- Identify essential and discretionary spending

- Understand spending patterns

- Make informed financial choices

Why Family Budgets Matter

Budgeting isn’t about restricting your spending. It’s about empowering your family to make smart financial decisions. A well-crafted budget helps you:

- Align spending with family goals

- Reduce financial stress

- Build long term financial stability

Creating Financial Clarity

A family budget transforms abstract financial concepts into concrete plans. By mapping out your financial resources, you gain control and confidence. You can spot potential savings, cut unnecessary expenses, and strategically allocate funds toward important family priorities.

Read more about budget tracking techniques to enhance your financial planning skills and create a robust financial strategy for your household.

Why Family Budgets Matter for Financial Health

Family budgets are not just financial documents they are powerful tools for securing your family’s long-term financial well-being. Government consumer resources emphasize the critical role budgets play in managing household finances effectively.

Financial Stability Through Intentional Planning

A family budget acts as a financial compass, guiding households through complex economic landscapes. By creating a clear roadmap of income and expenses, families can make strategic decisions that protect their financial future. This intentional approach helps prevent financial surprises and reduces the stress associated with unexpected monetary challenges.

Key benefits of consistent budgeting include:

- Creating a safety net for emergencies

- Identifying unnecessary spending patterns

- Establishing clear financial goals

- Reducing overall financial anxiety

Breaking the Paycheck to Paycheck Cycle

Many families find themselves trapped in a continuous cycle of financial uncertainty. Learn strategies to break the paycheck-to-paycheck cycle and transform your financial narrative. Budgeting provides a structured approach to understanding your spending habits, allowing you to redirect funds toward savings and long-term financial objectives.

Building Financial Confidence

Budgeting is more than number crunching. It’s about creating financial empowerment for your entire family. When everyone understands the household’s financial strategy, it promotes transparency, shared responsibility, and collective financial growth. By involving family members in budget discussions, you teach valuable financial literacy skills that will benefit them throughout their lives.

How a Family Budget Works: Basics Explained

Understanding how a family budget functions is like having a financial GPS that guides your household toward economic stability. Financial management research reveals that successful budgeting requires strategic planning and consistent tracking.

Core Components of a Family Budget

A family budget operates through several fundamental elements that work together to create a comprehensive financial picture. These components transform abstract financial concepts into practical, actionable strategies. The primary building blocks include:

- Income tracking: Documenting all sources of household revenue

- Expense categorization: Classifying spending into essential and discretionary categories

- Financial goal setting: Establishing short and long-term monetary objectives

Budgeting Mechanics: Money Movement

Budget mechanics involve understanding how money flows through your household. This means carefully monitoring income streams and systematically allocating funds across different financial priorities. Learn practical steps to start your budget and gain control over your financial landscape.

The process typically involves:

- Calculating total monthly income

- Subtracting fixed expenses like rent or mortgage

- Allocating funds for savings and emergency reserves

- Managing discretionary spending

Dynamic Financial Planning

A budget is not a static document but a living financial strategy that adapts to changing family circumstances. Successful budgeting requires regular review and adjustment. By treating your budget as a flexible tool, you can respond to unexpected expenses, changing income levels, and evolving family needs.

Below is a table that organizes the core components of a family budget and their brief explanations to help clarify their roles in household financial planning.

| Component | Description |

|---|---|

| Income Tracking | Monitoring all household income sources, including salary and others |

| Expense Categorization | Dividing spending into essential and discretionary categories |

| Financial Goal Setting | Establishing both short-term and long-term financial objectives |

| Budget Review & Adjustment | Regularly updating the budget to reflect changes in circumstances |

| Savings Allocation | Setting aside funds for emergencies and future needs |

| Family Involvement | Including all members in budgeting to promote transparency |

Components of a Family Budget: Income and Expenses

A successful family budget is built on understanding two fundamental financial elements: income and expenses. Family financial planning experts emphasize the importance of comprehensive tracking and strategic allocation of household resources.

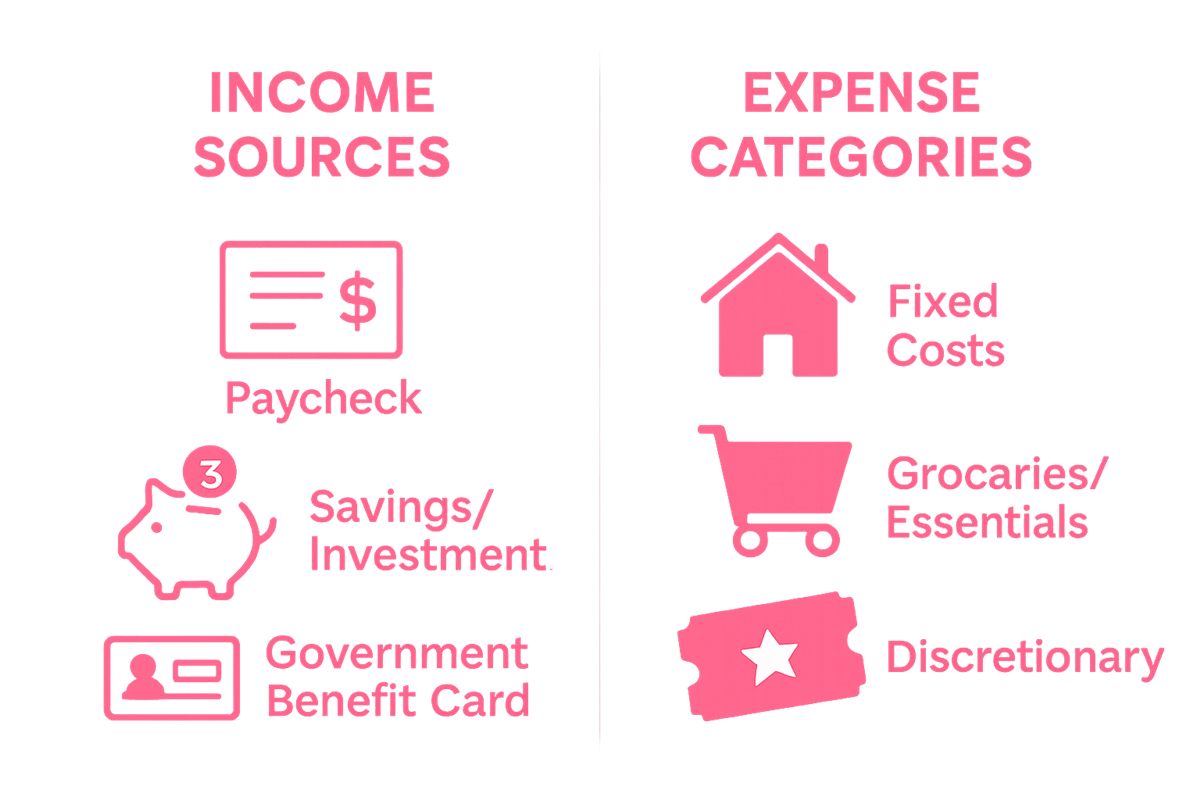

Understanding Income Sources

Income represents all financial resources entering your household. This goes beyond just salary and includes multiple potential revenue streams. Comprehensive income tracking means capturing:

- Primary employment earnings

- Secondary job or freelance income

- Investment returns

- Passive income like rental properties

- Government benefits or support payments

Categorizing Household Expenses

Expenses are the financial outflows that impact your family’s budget. Learn smart strategies for managing family food costs to control one of the most significant spending categories. Expenses typically fall into two primary categories:

- Fixed Expenses: Consistent monthly costs like

- Mortgage or rent

- Utilities

- Insurance premiums

- Car payments

- Variable Expenses: Fluctuating costs such as

- Groceries

- Entertainment

- Clothing

- Discretionary spending

Balancing Financial Ecosystem

The relationship between income and expenses creates your household’s financial ecosystem. Successful budgeting means ensuring your income consistently exceeds or matches your total expenses. This balance prevents debt accumulation and allows for strategic savings.

The following table categorizes typical sources of household income and expense types, summarizing their characteristics for easier comparison and tracking.

| Category | Examples | Notes |

|---|---|---|

| Income | Salary, Freelance, Investments, Benefits | All cash inflow sources in the household |

| Fixed Expenses | Mortgage, Utilities, Insurance, Car Payment | Consistent, predictable monthly outflows |

| Variable Expenses | Groceries, Entertainment, Clothing, Miscellaneous | Fluctuate from month to month |

By meticulously tracking both income sources and expense categories, families can create a robust financial framework that supports current needs while preparing for future goals.

By meticulously tracking both income sources and expense categories, families can create a robust financial framework that supports current needs while preparing for future goals.

Real-World Examples of Family Budgets in Action

Transforming financial theory into practical strategy requires seeing how real families navigate budgeting challenges. Family financial adaptation research demonstrates that successful budgeting is about flexibility and strategic planning.

Young Family Budget Scenario

Consider the Johnson family. With two young children and a combined annual income of $75,000, they face complex financial demands. Their budget breakdown illustrates practical budgeting in action:

- Monthly Income: $6,250

- Fixed Expenses:

- Mortgage: $1,800

- Utilities: $350

- Car Payment: $400

- Insurance: $250

- Variable Expenses:

- Groceries: $800

- Childcare: $1,200

- Entertainment: $300

- Miscellaneous: $250

Adapting to Financial Challenges

Discover budget-friendly family meal strategies that can help reduce one of the most significant household expenses. The Johnsons demonstrate how families can adjust when unexpected expenses arise. By maintaining an emergency fund and regularly reviewing their budget, they create financial resilience.

Key adaptive strategies include:

- Reducing discretionary spending during tight months

- Reallocating funds from entertainment to savings

- Seeking additional income opportunities

Continuous Budget Refinement

Successful family budgeting is not a one-time event but an ongoing process of financial learning and adjustment. The most effective budgets evolve with changing family circumstances, income shifts, and emerging financial goals. By treating their budget as a dynamic tool, families like the Johnsons transform financial planning from a rigid spreadsheet into a responsive strategy that supports their unique needs and aspirations.

Ready to Take Control of Your Family Budget?

Struggling with unpredictable expenses and constant financial stress can be overwhelming for any family. In “Understanding What is a Family Budget: A Clear Guide,” you learned how mapping out income and expenses creates a sense of clarity and stability for your household. But even with a detailed plan, real-life challenges like cutting overspending, organizing bills, and balancing priorities can leave you feeling stuck.

Take the next step and turn your budget into real results. Unlock simple living strategies, proven budgeting systems, and family-oriented organization solutions designed to help you reach your savings goals, avoid financial surprises, and finally find peace of mind. Explore more proven tools to begin transforming your home and your finances today. Your path toward a balanced and confident financial future starts here.

Recommended

- Understanding Your Budget Tracking Guide for Families –

- How to Feed a Family on a Budget –

- How to Start a Budget (When you don’t know where to start) –

- easy budget –

Want a little more help with this? Grab my free Finance & Life Planner over on the Free Resources page — and when you’re ready to go deeper, the First Budget in 30 Minutes will carry you the rest of the way.